All Categories

Featured

Table of Contents

Comprehending the Modern Design of 2026 Credit Reports

Reading a credit report in 2026 includes browsing a more complicated range of information than previous generations came across. While the three-digit score stays a fast referral point, the underlying information offer the genuine story of financial health. A lot of reports are now divided into distinct areas that track whatever from traditional loan repayments to alternative information like repeating membership services and rental history. For homeowners in Free Credit Counseling Session, keeping a close eye on these information is the main defense against identity theft and clerical mistakes.The recognition area remains the first obstacle. It contains names, addresses, and work history. In 2026, it prevails to see numerous variations of a name or previous addresses from across the region. Inconsistencies here are often the first sign of merged files or deceitful activity. Beyond standard ID, the report notes tradelines, which are the private accounts accepted lenders. Each tradeline displays the date opened, the credit line or loan quantity, the present balance, and a 2026 payment status.

Customer Rights and Monitoring in Your Region

Federal defenses have actually expanded to fulfill the needs of a digital-first economy. Every customer in the United States preserves the right to contest any information that is not precise, total, or verifiable. Under upgraded guidelines, credit bureaus should investigate these claims within a specific window, generally thirty days. Interest in Debt Relief has actually grown as information security becomes a top concern for those keeping an eye on these files.Monitoring is no longer a passive activity carried out once a year. In 2026, weekly access to reports has actually become the requirement for maintaining a precise profile. This frequency allows individuals to catch unapproved inquiries-- requests made by loan providers to view a file-- before they lead to fraudulent accounts. High numbers of "hard" queries can lower a score, while "soft" queries, such as those used for pre-approved deals, do not impact the total. Professional Debt Relief Services supplies the necessary oversight for those seeking to enhance their standing before obtaining major loans.

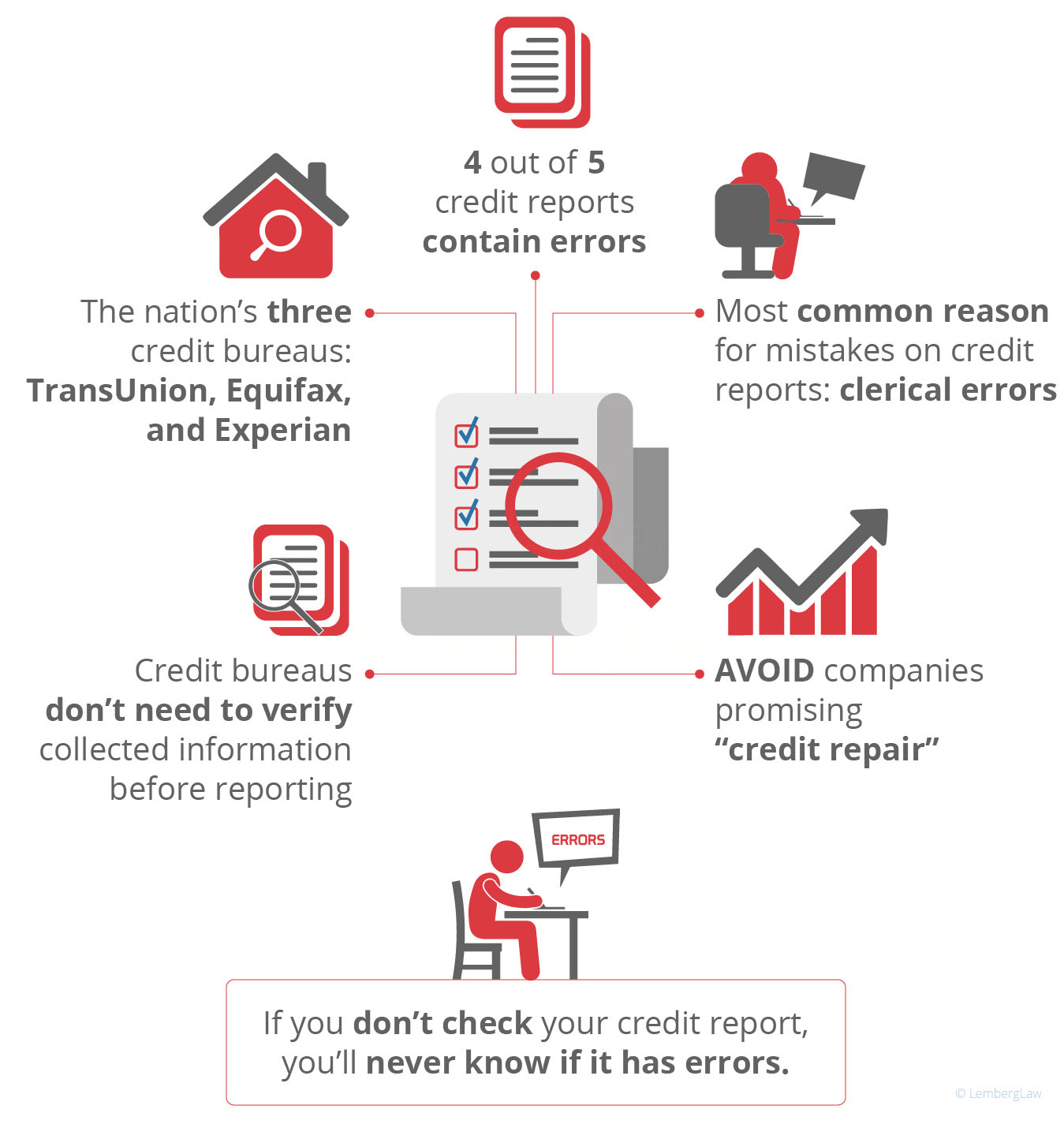

Recognizing and Contesting Mistakes

Errors on a credit report can vary from a misspelled street name in Free Credit Counseling Session to a paid-off debt looking like past due. When an error is discovered, the dispute process ought to be initiated with both the credit bureau and the particular creditor that offered the information. Keeping records of all correspondence is a requirement for a successful resolution. Documentation such as bank declarations from earlier in 2026 or "paid in full" letters serves as proof throughout these investigations.The effect of a single mistake is considerable. A late payment reported in mistake can drop a rating by lots of points, possibly causing greater insurance premiums or declined rental applications. Homeowners frequently search for Debt Relief in Florida when they experience persistent mistakes on their month-to-month statements that the bureaus stop working to correct.

The Function of Nonprofit Credit Therapy in 2026

For those having problem with the contents of their report, Department of Justice-approved 501(c)(3) not-for-profit firms use a path toward stability. These organizations supply free credit counseling and HUD-approved real estate therapy. They run across the country, guaranteeing that people in any given area have access to expert assistance without the high fees connected with for-profit repair companies.One of the most reliable tools provided by these nonprofits is the financial obligation management program. This program combines different regular monthly commitments into a single payment. Agencies negotiate with lenders to minimize rates of interest, which helps the participant pay down the principal balance quicker. This systematic method shows up on a 2026 credit report as a series of on-time payments, which is the most prominent consider a credit score.

Financial Literacy and Financial Obligation Management

A credit report is a reflection of previous habits, but monetary literacy education helps shape future results. Lots of neighborhood groups and banks partner with nonprofits to supply workshops on budgeting and financial obligation reduction. These programs are customized to the specific economic conditions of the surrounding area, helping consumers understand how to manage inflation and shifting interest rates.Pre-bankruptcy therapy and pre-discharge debtor education are also necessary actions for those required to look for legal debt relief. These sessions guarantee that individuals comprehend the long-lasting effects of insolvency on their credit report and find out the abilities required to restore after the procedure is completed. By concentrating on education instead of just fast fixes, these firms help produce long lasting financial stability.

Keeping Long-Term Credit Health

Achieving a high credit report in 2026 requires a mix of discipline and regular upkeep. Utilizing less than 30% of readily available credit line, a principle called credit utilization, remains a key technique. If a credit card in Free Credit Counseling Session has a limitation of $5,000, keeping the balance listed below $1,500 is typically encouraged. In addition, the age of accounts matters; keeping older accounts open, even if they are not utilized often, assists increase the typical length of credit history.Strategic credit building likewise includes diversifying the types of accounts on a report. A healthy mix may consist of a home loan, an auto loan, and a few revolving credit cards. In 2026, some bureaus likewise factor in "increase" information, where consumers opt-in to include utility and phone payments in their rating estimation. This is particularly handy for more youthful individuals or those in diverse communities who are just starting to establish their financial footprint.Regularly decoding the details of a credit report makes sure that a customer is never amazed by a loan rejection. By understanding the data, exercising legal rights to accuracy, and using nonprofit resources when financial obligation ends up being uncontrollable, individuals can keep control over their monetary track records throughout 2026 and beyond.

{kind=link}

Latest Posts

Analyzing 2026 Personal Bankruptcy Eligibility for Your State

Browsing the Complexity of Modern Credit Reporting Laws

Improving Your Score by Targeting Local Reporting Errors